How to Pay Creators Globally Without Building a Banking Team

If your creator roster spans Southeast Asia, the Middle East, and beyond, paying them across borders isn't just a payments problem.

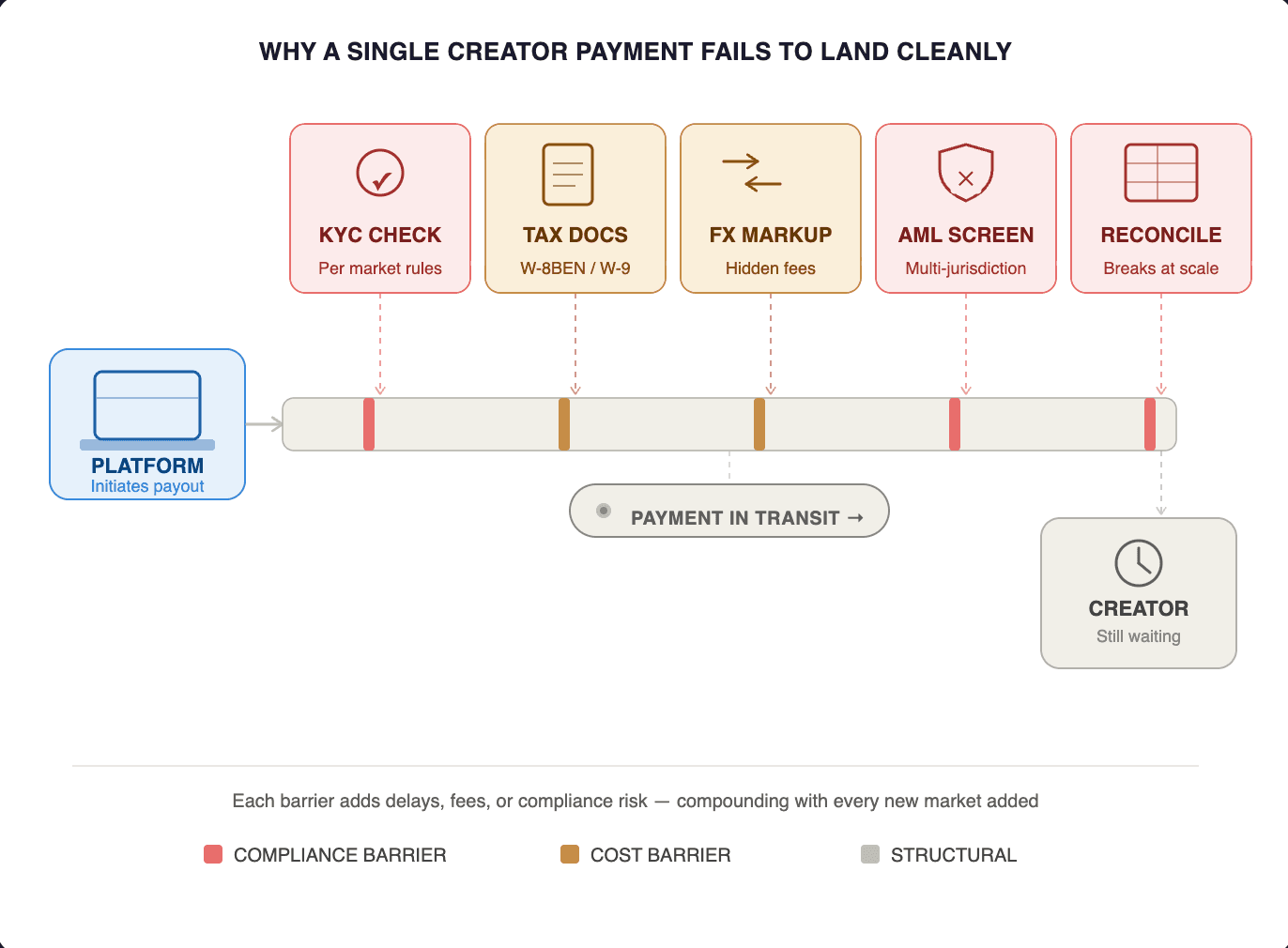

It's a compliance problem. A KYC problem. A tax documentation problem. A reconciliation problem that compounds with every market you add and every creator you onboard. For creator platforms managing talent across multiple countries, the operational challenge is the same everywhere — and it compounds with scale.

And if you're solving it manually, you're not just inefficient. You're building a quiet case for your best creators to look elsewhere.

The problem isn't just slow. It's structurally expensive.

High fees, slow processing times, and complex compliance requirements mean many creators lose 5–15% of their earnings just moving money across borders. For a creator earning $50,000 annually, that's up to $7,500 disappearing in fees, FX markups, and processing delays they didn't agree to and often can't see.

According to InfluenceFlow's 2025 payment processing guide, 47% of influencer disputes stem directly from payment delays or misunderstandings — making payment infrastructure one of the highest-leverage problems a platform can solve.

The retention cost of broken payout infrastructure is real — we covered why slow payouts are the primary driver of creator churn in detail here.

Creators who consistently receive less than expected don't file formal complaints. They quietly reduce their commitment to your platform, hedge with alternatives, and eventually anchor their business somewhere that pays them cleanly and completely.

Why global creator payments are genuinely hard to build

The instinct is to solve this with a payments provider. Add Stripe. Add PayPal. Wire transfers for the larger markets. It works at 10 creators. At 100, the cracks show. At 1,000, it breaks.

Here's what actually has to work for a global creator payment to land cleanly:

KYC and identity verification — every creator in every market needs to be verified before they can receive funds. KYC procedures that satisfy one country's rules may not meet another's. This regulatory diversity slows onboarding and raises operational costs. Across Singapore, the Philippines, Indonesia, and the UAE simultaneously, that's four different frameworks handled manually, by default.

Tax documentation — W-8BEN forms for international creators, W-9s for US-based ones, local reporting obligations in each jurisdiction. Managing this manually across any meaningful creator roster is a full-time compliance function.

FX conversion — traditional banks often embed large markups in the exchange rate while layering on transaction fees, making it hard to predict or control costs. Creators in local markets see a number that's smaller than expected. The trust deficit compounds silently.

AML and sanctions screening — global payments must satisfy multiple countries' AML and counter-terrorism financing regulations. Each intermediary may apply checks, meaning the same payment gets screened repeatedly, driving up compliance complexity.

Reconciliation — at scale, the volume of transactions across multiple corridors, currencies, and payment rails creates a problem that spreadsheets cannot solve. Managing payments to 5 creators is workable manually. At 500+, you need infrastructure with fraud detection, reconciliation, and dispute management built in.

Solving all five simultaneously, across global markets, without a dedicated banking and compliance team, has historically seemed structurally impossible. That's precisely why so many creator platforms are still on Net-30.

What the platforms solving this are doing differently

The platforms pulling ahead have made one specific decision: they stopped trying to build this themselves and started treating payout infrastructure as something to embed, not to own.

In practice, that means accessing global cross-border payouts, KYC, FX management, and card issuance through a single creator payout API suite — without new bank contracts per country, without a compliance team per market, and without an 18-month build cycle.

The operational difference is immediate:

Creator onboarding goes from days and weeks to minutes. Digital KYC handles identity verification at sign-up across multiple countries.

FX and settlement becomes transparent. Creators receive consistent, predictable amounts. The trust deficit disappears.

Compliance coverage — AML screening, sanctions checking, regulatory reporting — operates under a licensed umbrella. Licensed, Visa and Mastercard authorised, PCI DSS certified.

Reconciliation is automated. Every transaction is tracked. Every payout verified.

What this looks like in practice

One platform in the creator economy manages enterprise B2B transactions alongside mass payouts to thousands of influencers across Asia, North America, and beyond. The infrastructure requirement was the same in both cases: instant, reliable settlement, compliant in every market, without building separate banking relationships per corridor.

By embedding MatchMove's Banking Wallet OS™ through API integration, the platform went live across 200+ countries without negotiating new bank contracts, without hiring compliance teams per jurisdiction, and without the 18-month build that kind of coverage had historically required. Creators went from sign-up to pay-ready in minutes.

The revenue angle most platforms miss

Cross-border payout infrastructure is almost universally treated as a cost line. It doesn't have to be.

Platforms that issue branded creator cards — co-branded Visa or Mastercard under the platform name — earn interchange revenue on every transaction. Every time a creator uses their platform card to pay a contractor, book a flight, or buy equipment, the platform earns. What was previously a pure cost becomes an ongoing revenue stream. The infrastructure pays for itself.

The practical question

If your platform manages creators globally and you're still handling KYC, tax documentation, FX conversion, and compliance through a patchwork of point solutions — the question isn't whether to fix it. It's how fast you can.

The platforms that moved on this are already compounding the advantage. Their creators are onboarded faster, paid more reliably, and financially embedded in ways that make switching structurally costly.

The ones still managing this manually are funding that advantage — one delayed payment at a time.

MatchMove's Banking Wallet OS™ gives creator platforms instant payouts, co-branded Visa and Mastercard creator cards, digital wallets, and KYC — through secure and scalable APIs, without building a banking team or negotiating a single bank contract. A single integration covers global cross-border payouts, KYC, and compliance across 200+ countries — and platforms go live in 8 – 12 weeks.

Common questions about global creator payments

Do I need a local bank account to pay creators in each country?

No. Embedded finance infrastructure comes with pre-existing banking relationships and regulatory coverage built in — across multiple countries. You connect once through a single API. The local banking infrastructure is already there.

What tax forms are required for international creator payments?

The most common requirements are W-8BEN for non-US creators receiving payments from US platforms, and W-9 for US-based creators. Multi-jurisdiction reporting obligations vary by market.

How does digital KYC work for cross-border creator onboarding?

Creators submit identity documents at sign-up. Digital verification checks them against local KYC requirements in their market — no manual review queue, no jurisdiction-specific document chasing. Most creators go from sign-up to pay-ready in minutes.

Sources: InfluenceFlow International Creator Payments Guide 2025 · InfluenceFlow Influencer Payment Processing Guide 2025 · Convera Cross-Border Payments Challenges 2025 · Rapyd Top 8 Cross-Border Payment Challenges 2025 · ACI Worldwide Cross-Border Payments Landscape 2025